A Concrete Contractor’s Read on Hyperscaler Earnings: The AI Buildout Is Still Hitting the Ground

No end in sight. | OpenAI

The latest earnings reports from Amazon, Microsoft, and Alphabet were released on April 29, 2026, and they tell a pretty simple story for the concrete industry.

The AI data center buildout is not slowing down yet.

Wall Street can argue about margins, stock prices, capex discipline, and whether all this AI spending will pay off. That is their lane. Our lane is different. We care about whether these companies are still spending money on the physical world.

Are they still building? Are they still short on capacity? Are they still signing customers that require more compute? Are they still fighting power constraints? Are they still buying land, equipment, cooling systems, substations, generators, and everything else that eventually needs concrete under it, around it, or protecting it?

Based on the latest earnings reports from AWS, Microsoft, and Google, the answer is yes.

These companies all reported strong cloud growth tied to AI demand. They also reported or discussed massive capital spending plans. That matters because AI is not just software floating around in the sky. It runs inside very real buildings, on very real land, connected to very real power infrastructure. That means foundations, slabs, duct banks, equipment pads, generator yards, cooling infrastructure, switchgear pads, utility corridors, paving, stormwater structures, and a whole lot of schedule pressure.

The concrete industry should be paying attention.

The numbers are too big to ignore

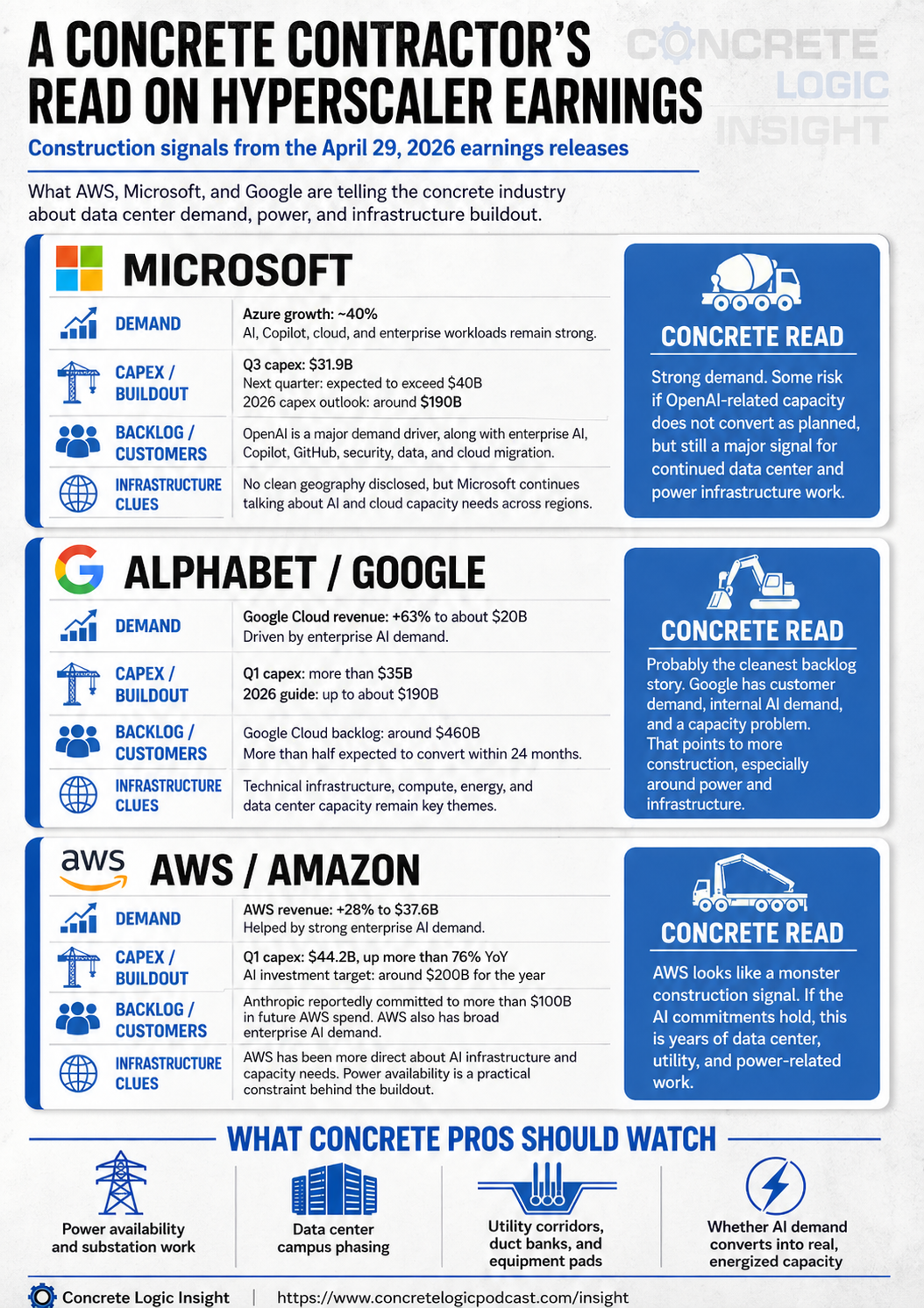

Microsoft reported Azure growth of about 40%, but investors focused heavily on the company’s capex. Microsoft’s quarterly capital expenditures were reported at $31.9 billion, up sharply from the prior year, with expectations for capex to exceed $40 billion next quarter and reach around $190 billion for the year.

That is not a normal maintenance budget.

That is an infrastructure buildout.

Alphabet’s Google Cloud business grew even faster. Google Cloud revenue jumped 63% to around $20 billion, and Alphabet’s cloud backlog reportedly reached about $460 billion, with more than half expected to convert within the next 24 months. Alphabet also spent more than $35 billion in Q1 capex and guided toward as much as $190 billion for the year.

AWS grew 28% to $37.6 billion, its fastest growth in several quarters, and Amazon’s Q1 capital expenditures were reported at $44.2 billion, up more than 76% year over year. Amazon also pointed to a roughly $200 billion AI investment target for the year.

That is the headline for construction.

These companies are not talking like they have too much capacity. They are talking like they still need more.

What the reports are really saying to contractors

The mistake would be to look at these reports like a stock analyst. A concrete contractor does not need to predict whether Microsoft’s stock is going up next week or whether Amazon’s margins beat expectations.

The better question is this:

Do these earnings reports point to more physical construction?

In my opinion, yes. But not every dollar of capex turns into concrete. A lot of this money goes to chips, servers, networking equipment, and other short-life technology assets. That part matters, but it is not our work.

The part we care about is the long-life infrastructure: data centers, power, cooling, site development, electrical infrastructure, buildings, foundations, and all the support systems around them.

The construction signal gets stronger when three things show up together.

Cloud revenue is growing.

The company says it is capacity constrained.

Backlog or customer commitments are large enough to justify more buildout.

All three showed up in these April 29, 2026 earnings reports.

Microsoft: strong demand, but OpenAI matters

Microsoft may have the most complicated story because of its deep relationship with OpenAI.

Azure grew about 40%, and Microsoft continues to show strong demand across cloud, AI, Copilot, GitHub, security, data, and enterprise workloads. That is important because it suggests Microsoft’s infrastructure demand is not only tied to one AI customer.

But OpenAI clearly matters.

If OpenAI continues to consume huge amounts of Azure capacity, Microsoft has every reason to keep building. If OpenAI slows, renegotiates, or fails to meet certain commitments, some future capacity decisions could get more scrutiny.

That does not mean Microsoft stops building data centers.

It means the next phase may get looked at harder.

For concrete contractors, Microsoft still looks like a major demand signal. But the best opportunities are likely tied to real campuses with secured power, active phasing, and clear capacity needs, not vague AI announcements.

Google: backlog is the story

Google may have the cleanest backlog story of the three.

Google Cloud revenue reportedly grew 63% to around $20 billion, and Alphabet’s cloud backlog was reported around $460 billion. More than half of that backlog is expected to convert within 24 months.

That is a big deal.

Backlog does not automatically equal new concrete tomorrow, but it does tell us something important. Google has customer demand that needs infrastructure. If they do not have enough compute capacity, they cannot turn that demand into revenue as quickly as they want.

That makes data centers a revenue problem, not just a real estate problem.

Google also has its own internal demand. Gemini, Search, YouTube, cloud storage, enterprise AI, and TPU-related demand all pull on the same technical infrastructure. That means Google’s data center need is not only driven by outside customers. It is also driven by Google’s own products.

For concrete contractors, Google’s report points to continued opportunity around data center campuses, technical infrastructure, power, cooling, and site development. The backlog makes this feel less like hype and more like a capacity problem that has to be solved.

AWS: maybe the clearest construction signal

AWS may be the most direct construction story.

AWS revenue grew 28% to $37.6 billion, and Amazon’s Q1 capex reportedly hit $44.2 billion, up more than 76% year over year. Amazon also pointed to massive AI infrastructure investment and large customer commitments.

The customer clues matter here.

AWS has demand tied to Anthropic, OpenAI, Meta, Uber, and a long list of enterprise customers. Some of those commitments are not normal cloud workloads. They are power-hungry AI workloads that require serious compute capacity.

That is where the construction signal gets loud.

When cloud demand is measured in large AI commitments and major compute capacity, the physical requirements follow: land, power, cooling, substations, duct banks, foundations, equipment pads, generator yards, utility corridors, and heavy sitework.

AWS looks like a strong multi-year construction signal if those customer commitments hold.

The risk is that some AI commitments may not convert exactly as announced. If a major customer slows down or changes direction, AWS could delay future phases, reassign capacity, or adjust timing. But with broad enterprise demand and multiple large AI customers, AWS does not look like a one-customer story.

The real bottleneck may not be concrete

Here is where concrete contractors need to be honest.

Concrete is important, but it may not be the main bottleneck.

Power is.

These hyperscalers are fighting for energy, grid capacity, switchgear, transformers, substations, generators, and electrical infrastructure. Data centers do not matter much if they cannot be energized.

That is why the concrete opportunity is not just the data center building itself. It is the whole power ecosystem around it.

That includes substation foundations, transformer pads, generator yards, duct banks, utility vaults, battery energy storage foundations, cooling equipment pads, heavy paving, stormwater structures, retaining walls, site concrete, slabs, and foundations inside the data center campus.

The contractors who understand that full package will have an advantage.

The ones just chasing the building slab may miss a lot of the work.

The risk: not every AI headline turns into immediate construction

There is a risk here, and it should not be ignored.

Some of this demand is based on long-term AI commitments. If a customer like OpenAI, Anthropic, or another AI company does not use the capacity as planned, the hyperscaler may slow down future phases. They may delay fit-out. They may hold the shell and wait. They may reassign capacity to another customer. They may value engineer the next campus.

That does not mean the whole market collapses. But it could create starts and stops.

For contractors, that means the risk is not just whether there will be work. The risk is how the work gets released.

Fast one month.

Frozen the next.

Then suddenly urgent again because equipment is arriving and the owner wants revenue-ready capacity.

That is a hard way to build.

Concrete contractors should pay attention to whether a project has signed customer demand, secured power, utility commitments, long-lead electrical gear ordered, a real construction schedule, a phased campus plan, and a clear path to energization.

A data center without power is just an expensive warehouse full of promises.

What this means for the concrete industry

The concrete industry should be looking at hyperscaler earnings the same way it looks at cement shipments, rebar pricing, diesel costs, and project backlogs.

These reports are demand signals.

When Microsoft, Google, and AWS say they are spending tens of billions of dollars on cloud and AI infrastructure, that should get our attention. When they say demand is strong and capacity is tight, that should get even more attention. When they start talking about energy, data center operations costs, backlog, and multi-year customer commitments, that is a signal for contractors, ready-mix producers, rebar suppliers, formwork companies, pump companies, and testing labs.

This is not just a tech story.

It is a construction story.

But it is a construction story with a different kind of owner. These owners are not building because they want a nice building. They are building because every day of delayed capacity may mean delayed revenue.

That changes the pressure on the job.

Schedule matters. Power matters. Coordination matters. Early planning matters. Ready-mix availability matters. Rebar congestion matters. Embed layout matters. Cooling equipment pads matter. Duct bank sequencing matters. Testing delays matter.

Everything that slows down the path to energized, revenue-producing capacity becomes a business problem.

The blunt takeaway

The April 29, 2026 earnings reports from AWS, Microsoft, and Google point to continued demand for data center and power-related construction.

The capex numbers are massive. The cloud growth is real. The backlog is real. The capacity pressure is real.

But contractors should not assume every AI headline turns into immediate concrete work.

The smart move is to watch the details. Look for projects with secured power, signed demand, real phasing, and owners who need capacity online fast.

That is where the real opportunity is.

The AI boom may live in the cloud.

But the cloud still needs concrete.

Sources

Microsoft FY2026 Q3 earnings release and investor materials

https://www.microsoft.com/en-us/investor/earnings/fy-2026-q3/press-release-webcast

https://www.microsoft.com/en-us/investor/events/fy-2026/earnings-fy-2026-q3

Amazon Q1 2026 earnings release

https://ir.aboutamazon.com/news-release/news-release-details/2026/Amazon-com-Announces-First-Quarter-Results/

Alphabet Q1 2026 earnings release / SEC filing

https://www.sec.gov/Archives/edgar/data/1652044/000165204426000043/googexhibit991q12026.htm

Reuters coverage of Alphabet earnings

https://www.reuters.com/business/alphabets-cloud-unit-beats-quarterly-revenue-estimates-strong-ai-demand-2026-04-29/

Reuters coverage of Amazon earnings

https://www.reuters.com/business/retail-consumer/amazon-beats-quarterly-cloud-growth-estimates-2026-04-29/

Barron’s coverage of Microsoft earnings

https://www.barrons.com/articles/microsoft-earnings-stock-price-1750a2b4

Who pays a 50% tariff on Canadian cement?